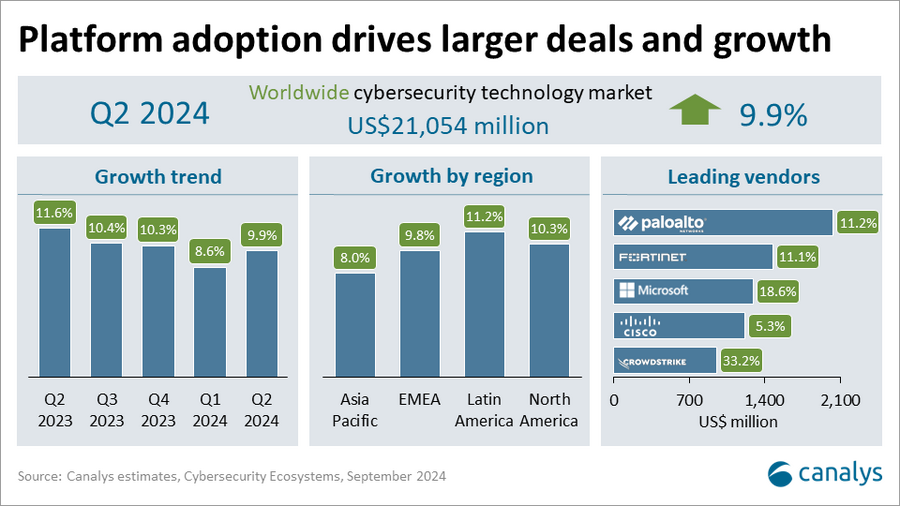

Cybersecurity spending was boosted by larger deals in Q2 2024, as vendors focused on cross-selling their platforms. This is despite customers scrutinizing budgets and taking longer to sign off on deals due to ongoing macroeconomic uncertainty. Political disruption from elections around the world also affected spending in the public sector. Nevertheless, the worldwide cybersecurity technology market grew 9.9% year on year to US$21.1 billion. This growth, while slightly below Canalys’ best-case forecast, highlights the ongoing prioritization of cybersecurity.

The top 12 vendors benefited the most from customers taking early steps to transitioning to platforms. Collectively, they accounted for 53.2% of total spending in Q2 2024, up from 51.9% last year. Palo Alto Networks (+11.2%) extended its leading market share, driven by uptake of its Prisma Cloud, Cortex for SecOps, network security software and SASE. Its acquisition of IBM’s QRadar assets will help boost its platformization strategy. Fortinet (+11.1%) ranked second. Its growth re-accelerated in Q2 as its pivot to SecOps and SASE boosted its results, while signs of a firewall recovery emerged. Microsoft (+18.6%) continued to gain share by focusing on platform adoption via E5 license enablement. Cisco (+5.3% excluding Splunk) completed its acquisition of Splunk, adding to its platform approach. CrowdStrike (+33.2%) made gains via customer adoption of its Falcon platform, though repercussions from the 19 July outage will hurt its future results.

Canalys Cybersecurity Market Pulse: Q2 2024

| Vendor | Market share Q2 2023 | Market share Q2 2024 | Revenue growth |

| Palo Alto Networks | 9.5% | 9.7% | 11.2% |

| Fortinet | 6.9% | 7.0% | 11.1% |

| Microsoft | 5.7% | 6.1% | 18.6% |

| Cisco | 6.0% | 5.8% | 5.3% |

| CrowdStrike | 3.7% | 4.5% | 33.2% |

| Okta | 3.4% | 3.6% | 16.6% |

| Check Point | 3.6% | 3.5% | 6.7% |

| Zscaler | 2.5% | 3.0% | 31.3% |

| Symantec | 2.9% | 2.7% | 3.2% |

| IBM | 2.7% | 2.5% | 2.5% |

| Trellix | 2.6% | 2.4% | 2.1% |

| Splunk | 2.4% | 2.4% | 13.5% |

| Others | 48.1% | 46.8% | 6.9% |

| All vendors | 100% | 100% | 9.9% |

“Organizations have been re-architecting their IT stacks for cloud and, more recently, for AI. They must also re-architect their cybersecurity to increase their resilience and counter the surge in ransomware attacks,” said Matthew Ball, Chief Analyst at Canalys. “Vendors are positioning their cybersecurity platforms to reduce customers’ complexity by consolidating redundant and legacy point products. But this also reduces organizations’ resilience by increasing dependency on fewer vendors. A balanced approach is needed.”

But platforms are more than just the single vendor solutions that most vendors are pushing today, with expanded product features and functions across cybersecurity. “Platform vendors must have an integration-first strategy, supporting a wide range of ISVs and simplifying multivendor procurement. They must support and enable an expanded ecosystem of transactional and service-led partners, particularly GSIs, MSSPs, MSPs and new types of partners, such as cyber-insurers. They must also reward their partners for innovation and value creation that ultimately drives customer demand for their platform,” said Ball.

Platform adoption will change how customers discover and buy cybersecurity technology and how they are supported via services. Channel partners will continue to play a vital role for both vendors and customers during and after this transition. Selecting the right vendor platform to build their business around will be one of the biggest long-term decisions partners need to make, because the vendor competitive landscape will change dramatically in the next three years. This will be one of the key discussion topics for senior leaders at vendors and channel partners during the cybersecurity Expert Hub sessions at the upcoming 2024 Canalys Forums in Berlin, Miami and Bali.

“Cybersecurity services will be more important than ever as customers look to their partners to advise, design, procure, build, adopt and manage their platform strategies,” said Srikara Upadhyaya, Research Analyst at Canalys. “For every dollar of cybersecurity technology spent by organizations this year, partners will generate US$1.90 on average from services, with managed security services, including MDR, incident response, managed SOC and technology, representing just over half of the opportunity. Cybersecurity services spending will grow 12.9% to US$163.3 billion this year.”

In Q2 2024, total cybersecurity technology spending through the channel accounted for 91.3%. Spending through systems integrators grew 9.3% and MSSPs increased 12.0%.

All regions grew in Q2, with growth rates improving in Asia Pacific (+8.0%) and EMEA (+9.8%). Growth in North America (+10.3%) remained robust, though it slowed from last quarter as recession concerns from rising unemployment affected economic confidence and levels of spending. Latin America (+11.2%) was the fastest-growing region.